|

MEC is excited to be providing you and your company with great discounts for all of your MLO education needs!

Click the links below to enroll at a steeply discounted rate!

|

|

Pre-Licensing EducationThe NMLS requires all licensed MLO's to take a minimum of 20 hours of pre-licensing education in order to obtain a license, as well as any state-required electives.

Need more information about obtaining a license? Visit our New MLO Licensing Guide |

Continuing EducationThe NMLS requires all licensed MLO's to take a minimum of 8 hours of continuing education each year, as well as any state-required electives.

We offer continuing education in a variety of formats. |

|

*Coupon Code: ORMPE* |

*Coupon Code: ORMCE* |

*Already have a license and need to add another state?: ORMPE* |

*Coupon Code: ORMCE* |

*Want a live instructor, but from the comfort of your own home? Limited Classes* |

*Want a live instructor, but from the comfort of your own home? Limited Classes* |

*PE Live Classroom instructions are limited* |

*CE Live Classroom instructions are limited* |

*Choose from our Test Prep and Tutoring options.* |

*We recommend calling the NMLS to see what may be required to reactivate your license.NMLS phone # 855-665-7123* |

|

To enroll over the phone or for live classes, please contact your account rep directly. Jason Carroll (801) 243-5409

Mortgage Educators and Compliance is excited to offer these incredible offers for NMLS-approved education. Restrictions apply. Limited time offer.

|

|

Refund Policy

Mortgage Broker vs Direct Lender: Comparing Career Paths & Benefits

So you're going into the business of being a mortgage lender. Good for you! Helping people get into their dream homes by helping in obtaining and closing loans that they need to do can be very rewarding.

But what part of the industry do you want to go into? Mortgage broker vs direct lender, that's the question. When considering a career in the mortgage industry, understanding the key differences between a mortgage broker and a direct lender is essential. In this comprehensive guide, we will explore these two distinct roles and their respective responsibilities within the home loan process.

Mortgage brokers act as intermediaries, facilitating communication between borrowers and multiple lenders to find competitive interest rates and loan programs. Originators of direct loans, e.g., banks and credit unions, present loans directly to borrowers without an intermediary.

We will delve into various aspects of both careers, such as fees associated with working with intermediaries versus direct lenders, comparing APRs (Annual Percentage Rates), fees, closing costs of different offers from both sources. Additionally, we'll discuss advantages and disadvantages of choosing either path based on individual circumstances.

By gaining an in-depth understanding of mortgage brokers vs direct lenders through this blog post, you'll be well-equipped to make informed decisions when pursuing your career in the mortgage industry.

Mortgage Broker vs Direct Lender: The Role of Mortgage Brokers

The mortgage broker acts as intermediaries between borrowers and lending institutions, helping people access financing for one of the biggest investments of their lives.

Connecting Borrowers with Lenders

Mortgage brokers facilitate the link between homebuyers and lending institutions, ensuring a loan tailored to the borrower's individual requirements that also meets with the lender's criteria.

Gathering Required Documentation

Mortgage brokers assist clients in gathering all necessary documentation required by lenders during the loan application process, including pay stubs, tax returns, bank statements, and credit reports.

Navigating Complex Mortgage Products

- Finding competitive rates: Brokers have access to multiple lenders, allowing them to find competitive interest rates for their clients based on individual circumstances.

- Evaluating different loan types: Brokers can help determine which loan option best suits each client's needs by comparing features like terms or payment structures.

- Identifying government-backed loans: Brokers can also help clients identify and apply for government-backed loans, such as FHA, VA or USDA mortgages, which may offer more favorable terms to eligible borrowers.

As a mortgage broker you can provide potential homebuyers with valuable insights and guidance throughout the entire loan process.

Mortgage Broker vs Direct Lender:

Direct Lenders in the Home Loan Process

The direct mortgage lender provides loans for homes directly to applicants without involving a mortgage broker, resulting in faster processing times and quicker decision-making.

These mortgage lenders have control over their own underwriting guidelines, allowing them to make funding decisions quickly and efficiently.

Companies like Better.com hold nationwide licenses, enabling them to process loans more quickly and efficiently than traditional banks or credit unions.

Homebuyers working with you as a loan officer at a direct mortgage lender can help them secure financing more quickly than those who work with mortgage brokers, who often rely on third-party approvals that can delay the process.

Understanding the differences between direct lenders and mortgage brokers is crucial for those looking to make a choice about what part of the industry to work in.

- Faster decision-making: Direct lenders are much faster at closing loans because they adhere strictly to their own established rules and procedures.

- Nationwide licensing: Companies like Better.com hold licenses in multiple states, allowing them to process loans more quickly and efficiently than traditional banks or credit unions.

Comparing Mortgages: Mortgage Broker vs Direct Lender

Choosing between a mortgage broker and a direct lender depends on your career goals and preferences.

Mortgage Brokers: Multiple Quotes in One Place

Brokers have access to various lending institutions, providing homebuyers with several loan options to compare rates, terms, and conditions.

Direct Lenders: Rates Based on Your Financial Profile

Working directly with a lender limits potential homebuyers to the loan products and rates of the lender you work for, which may not always be competitive due to factors such as the homebuyer's credit score, employment history, and down payment amount.

- Credit Score: Higher scores result in better rates since it indicates lower risk.

- Employment History: Stable job history is essential for eligibility and interest rates.

- Down Payment: Larger down payments can lead to better rates by reducing the loan-to-value ratio.

Fees Associated with Working with Intermediaries

As a mortgage broker, you do quite a bit of work beyond just looking up different interest rates, loan amounts and loan types. You will do a lot of research, this includes finding suitable loans based on specific needs and handling all required documentation until final approval has been granted by chosen providers.

Many people are distrustful of brokers due to their ability to assess a lot of hidden fees associated with their work. You'll want to be as transparent as possible with your clients so they understand exactly what they are paying you for.

Broker Fees and Charges for Assistance

As a mortgage broker you'll generally impose an origination commission or fee, varying from 1% to 2%, based on the loan sum. Some may also charge application or processing fees. However, mortgage brokers are required to disclose their fees upfront, so borrowers can make informed decisions about whether or not to work with them.

Importance of Hidden Costs

Thorough research before selecting either option is crucial when considering working as a mortgage broker or direct lender.

Asking questions of people working within different industry sectors and seeking recommendations from friends and family members who have recently gone down similar career paths can help you make a good decision. Either way, you'll always need to be sharp, honest, transparent and up to date with all relevant laws and policy in the mortgage business.

Remember, potential borrowers have more resources than ever that are helpful in their own research. Things like SmartAsset's free tool matches homebuyers up with three financial advisors in their area while helping compare mortgage rates from top lenders. When they come to you, assume they already know a lot.

- Shopping around: Homebuyers can obtain quotes from multiple brokers as well as direct lenders to ensure they're getting the best deal possible.

- Negotiating: A lot of homebuyers won't be afraid to negotiate lower fees if they feel they're too high - some brokers may need to be willing to reduce their charges in order to secure your business.

- Reading the fine print: Many homebuyers will understand all fees and charges associated with a mortgage broker's services before signing any agreements or contracts. Assuming this and acting accordingly will help you establish a reputation as honest and ethical.

With all of these resources available, what do mortgage lenders and brokers actually do? In this case, mortgage broker vs direct lender? It doesn't matter. Both can help ensure that homebuyers are taking the optimal route for their financial circumstances by thoroughly examining APRs, fees, and closing costs when evaluating offers. Do your homework and always be up to speed so that you can be the valuable source of knowledge and council that homebuyers are looking for.

Comparing APRs, Fees, and Closing Costs

If you become a broker comparing mortgage offers for clients, don't just focus on the interest rate - also compare APRs (Annual Percentage Rates), fees, and closing costs to help your clients make an informed decision. These are things that you will learn during the course of your education and licensure process but they're so important they bear repeating.

Analyzing different aspects of mortgage offers

- Interest Rate: The percentage charged on the borrowed amount.

- APR: Includes the interest rate and other costs like points, origination fees, and underwriting fees.

- Fees: Lenders may charge various fees like application or appraisal fees.

- Closing Costs: One-time expenses paid at closing include title insurance premiums, recording taxes, and escrow charges.

Compare mortgage rates, APRs, and costs from multiple sources to get the best deal.

Competitive options like SoFi's fixed-rate mortgages

If you prefer working for a direct lender, be aware of and be able to speak intelligently about SoFi's fixed-rate mortgage loans - they offer competitive rates and terms compared to other direct lender offerings. Remember to consider your unique financial situation, preferences, and long-term goals when choosing a mortgage option.

Brokers vs Direct Lenders: Pros and Cons

Weighing the pros and cons of working as a mortgage broker vs direct lender can be tricky, but being aware of the positives and negatives each offers can assist you in making an educated choice.

Pros & Cons Based on Individual Circumstances

- Mortgage Brokers: More independence, potentially higher earnings but brokerage can be fiercely competitive.

- Direct Lenders: More stability and job security but you'll work entirely within the confines of your employers policies.

Factors Influencing The Homebuyers Choice Between Broker Or Direct Lender

Credit score, loan type, and personal preferences can all play a role in deciding between a broker or direct lender.

- Credit Score: Improving your credit score can help secure better rates, but direct lenders may have stricter requirements.

- Loan Type: Certain loans may be more readily available through brokers.

- Personal Preferences: Consider communication style and desired level of assistance during the application process.

Ultimately, the choice between a mortgage broker vs direct lender depends on the homebuyer's unique needs and preferences. Give these considerations some thought and think about how your skills, career goals and preferences can be put to work in helping homebuyers make the best choices.

Common questions regarding Mortgage Broker vs Direct Lender

Mortgage Broker vs Direct Lender: Which is the better career choice?

It really depends on what your career goals and preferences are. Both a loan officer at a direct lender and a mortgage broker can help borrowers with the loan application, help them determine the correct loan amount and guide them through the whole process but they have different skill sets and tools to do so.

What Sets Mortgage Brokers Apart from Lenders?

- The mortgage broker acts on behalf of their clients and they have access to loans from multiple lenders, giving borrowers more choices.

- Brokers offer personalized attention, while lenders may prioritize quick approvals over individualized service.

Why Choose Mortgage Brokerage Over a Bank?

Mortgage brokers can offer more competitive rates and diverse loan programs than banks and can charge more for their services in doing that research.

Understanding the Difference Between Mortgage Brokers and Lenders

A mortgage broker acts as a middleman between borrowers and lenders, while direct lenders provide loans directly to borrowers. Brokers offer more choices, while lenders prioritize faster processing times.

Conclusion

When it comes to deciding on being a mortgage broker vs direct lender, knowing the difference between mortgage brokers and direct lenders is key. Mortgage brokers can offer multiple quotes and help navigate complex products, while direct lenders offer faster decision-making and nationwide licensing. However, it's important to consider your own personal situation, goals, preferences, risk tolerances, etc. before making a choice. Ultimately, the choice between a mortgage broker and direct lender depends on individual circumstances.

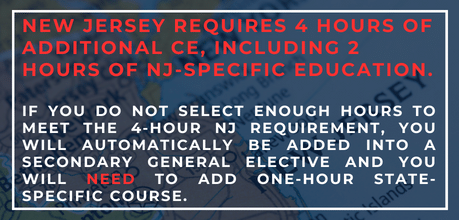

Select Your States To Purchase Below

Select Your State-Specific Electives To Purchase Below

|

Only state-specific CE hours will be added using this selector. Only states with additional state-specific CE hours will show. |

|

Mortgage Broker vs Direct Lender: Comparing Your Options

When it comes to securing a loan to cover your home purchase, the choice between working with a mortgage broker vs bank can be quite overwhelming. The mortgage business is complex. There are regular loans, jumbo loans, and USDA loans. Between the different loan products, mortgage rates and the loan application process can vary by lender. Both mortgage brokers and direct lenders can help you navigate the mortgage business.

Both routes present their own particular advantages and drawbacks which should be weighed by borrowers before settling on a choice. To help you make an informed decision about your mortgage options, this blog post will provide a detailed comparison of the advantages and disadvantages of working with mortgage brokers versus banks.

We'll discuss the pros and cons of working with a mortgage broker instead of the bank directly, as well as explore the benefits associated with obtaining loans directly from banks. Additionally, we will shed light on how brokers find suitable lending sources and outline fees associated with using their services.

Furthermore, we'll differentiate between direct lenders such as banks and credit unions (both physical and online lenders) versus correspondent lenders, highlighting key distinctions in terms of financial products offered by these institutions. We will also examine rebate pricing strategies employed by mortgage brokers due to not being tied down to one specific institution.

Lastly, we’ll guide you through factors affecting your decision-making process when choosing between a mortgage broker vs bank - including situations where working with a broker may prove advantageous for certain types of borrowers - followed by tips on researching reputable professionals within the industry.

When searching for home loans for a mortgage, it is wise to look at different loan providers such as brokers, firms, and direct lenders.

Mortgage Broker vs Bank

The mortgage application involves challenges. When looking for a mortgage, you can choose to work with either a broker or go directly through the bank. Working with your local bank or one of the big banks has pros and cons. Essentially, mortgage brokers are kind of like a real estate agent. They connect buyers and lenders. Mortgage brokers work with banks on your behalf but there are pros and cons to that approach as well.

Mortgage broker vs bank: Working with Mortgage Brokers

- Access to multiple lenders: Mortgage brokers work with various mortgage lenders and can compare offers for you. This gives you options for loan products to choose from when searching for the best rates and terms.

- Negotiation power: A good broker can help negotiate better interest rates, fees, and loan terms on your behalf since they are not tied to any specific lender.

- Potential savings: By comparing offers from multiple lenders, mortgage brokers may be able to secure lower rates or fewer fees than if you were dealing directly with one bank.

- Limited control over process: Some aspects of the loan application process may be out of their hands, potentially leading to delays or complications in securing financing.

Mortgage broker vs bank: Obtaining Loans From A Bank Directly

- Familiarity: If you already have an established relationship with your local bank or credit union and they provide you with multiple financial services, it might make sense to apply for a home loan through them.

- In-house services: Banks don't just offer home loans. Big banks and small ones offer additional financial services such as checking accounts, savings accounts, credit cards, and student loans, which can be convenient if you prefer to keep all your financial products in one place. Additionally, bank loan officers may have more flexibility during the loan approval process.

- Potential for better mortgage rates: Some banks may offer lower rates or other incentives to customers who have existing accounts with them.

- Limited options: When applying directly through a bank, you are limited to the loan programs they offer, which could mean fewer choices when it comes to interest rates and terms compared to working with a mortgage broker.

When searching for a mortgage, it is wise to look at different loan providers such as brokers, firms, and direct lenders.

Direct Lenders - Banks & Credit Unions

Banks and credit unions are financial institutions that offer loan options through their own institutions.

Correspondent lenders are brick-and-mortar banks that sell mortgages alongside other financial products such as checking accounts, savings accounts, and credit cards.

In-house approval process advantages

Direct lenders offer an in-house approval process, which can lead to a smoother and more efficient loan process compared to working with mortgage brokers who have to coordinate between multiple lenders.

- Fewer fees: Direct lenders often charge fewer fees than mortgage brokers.

- Potential discounts: Some banks may offer discounts on interest rates or closing costs if you're an existing customer or open new accounts with them during the home buying process.

- Easier communication: Dealing directly with one financial institution can make it easier to ask questions, resolve issues, and track progress throughout your loan application journey.

Faster funding decisions due to nationwide licensing

Banking establishments such as Wells Fargo, Bank of America, Chase, Rocket Mortgage (by Quicken Loans), USAA Federal Savings Bank (USAA), and Navy Federal Credit Union (NFCU) have their own bank loan officers and with them the capability to make speedy choices on loan applications because they are spread out over a vast area.

This can be particularly beneficial for first-time home buyers who may need faster approvals to secure their dream homes.

In general, opting for a direct lender such as banks or credit unions has several advantages when compared to using a mortgage broker in terms of obtaining a home loan.

However, it's essential to research both options thoroughly before making your decision. A home purchase is a big deal. Do your homework.

Loan Officers vs Mortgage Brokers

Loan officers and mortgage brokers may seem similar, but there are key differences that can impact your mortgage experience.

Comparing Commission Structures

Loan officers work for banks and earn commissions based on volume and profitability of loans originated, while mortgage brokers receive fees from borrowers and/or lenders upon successful completion of a loan transaction.

- Mortgage Brokers: May charge an origination fee or lender compensation.

- Loan Officers: Receive commission based on volume and profitability of loans originated.

Rebate Pricing Benefits

Mortgage brokers are able to provide competitive rates compared to direct lenders, such as banks or credit unions, which can be especially beneficial for those in unique financial circumstances.

Loan officers are limited to the mortgage options and mortgage rates provided by their employer.

Consider your individual requirements and inclinations before choosing which choice is best for you when obtaining a home loan.

Research Your Options Before Choosing Between Mortgage Brokers and Direct Lenders

It's crucial to research your options before choosing between mortgage brokers and direct lenders, as each has its unique pros and cons depending on individual circumstances and preferences.

Most first-time home buyers find their lender through online searches or recommendations based on reputation, quality, and service provided.

Ask Questions and Negotiate Fees/Points

Ask about the loan amount, interest rates, loan options, closing costs, prepayment penalties, application fees, points, and credit requirements for different loan programs.

Compare offers from multiple lenders, including big banks like Rocket Mortgage, to ensure you're getting the best deal possible.

Consider Your Credit History & Income/Assets

- Your creditworthiness is an essential factor to consider when selecting between different mortgage lenders.

- If your income fluctuates due to self-employment or if you have limited assets available for down payment/closing costs purposes, working with an experienced mortgage broker may prove more beneficial.

By researching your options and considering factors such as credit history, income/assets, and loan preferences, you can make an informed decision between mortgage brokers and direct lenders.

Remember that each option has its unique pros and cons, so weigh them carefully before making your final choice.

Choosing Between Mortgage Broker or Bank: Factors to Consider

Deciding between a mortgage broker or bank loan officer depends on your unique circumstances, such as credit history, financial stability, and preferences.

Access to Multiple Lenders vs Faster Funding Decisions

A mortgage broker can shop around for the best mortgage rates and terms from multiple lenders, while banks may offer faster funding decisions due to their in-house approval process.

Personalized Service vs Established Banking Relationships

- Mortgage Brokers: A good broker provides personalized service tailored to your situation, guiding you through the application process and negotiating better mortgage rates on your behalf.

- Banks: If you have an established relationship with a bank, you may receive discounts on fees or lower interest rates for using their services for mortgages, student loans and other financial products.

Research both options thoroughly before making a decision, considering factors such as access to multiple mortgage companies, personalized service, faster funding decisions, and existing banking relationships.

Common questions about a Mortgage Broker vs Bank

Mortgage Broker vs Bank: Which is Better?

It depends on your needs, but a mortgage broker can offer more options from multiple lenders, while banks provide direct lending with potentially fewer fees.

Is it Easier to Get a Mortgage with a Broker or Bank?

Either way, the mortgage application involves challenges. Mortgage brokers can make the process easier by shopping around for the best rates, but those with strong credit scores might find comparable deals directly through banks or credit unions.

Mortgage Broker vs Bank: What's the Difference?

Bankers offer loans directly from their employer, while brokers work independently to connect borrowers with suitable loans from multiple lenders.

Why Work with a Mortgage Broker?

Mortgage brokers have access to numerous loan programs and competitive rates across different lenders, making them especially helpful for borrowers with unique circumstances like being self-employed or having low credit scores.

Looking for more information on mortgage brokers? Check out Investopedia's guide to mortgage brokers.

Conclusion

Choosing between a mortgage broker and a bank for your home loan can be a tough decision, but understanding the pros and cons of each can help.

- Mortgage brokers offer access to multiple lending sources, but watch out for those fees.

- Banks provide direct lending services and lower interest rates, but you're limited to their offerings.

Ultimately, your choice will depend on factors like credit score, loan amount, and specific needs, so do your research and choose wisely.

For more information on mortgages and loans, check out these credible sources: